In a nutshell you to definitely less than specific affairs, particularly reduced deals, you will need a permit is a lender otherwise representative inside the Iowa. But when you manage mainly larger deals (over $58,three hundred, as of 2020), or you perform generate fewer than ten purchases a year, you don’t need to check in.

Others significant items: a loan representative might not evaluate or gather an advance commission before the representative successfully procures financing on the debtor. Iowa Code Part 535C.2A (2021). Ticket associated with the law is actually a beneficial “severe misdemeanor”. Iowa Password Chapter 535C.6 (2021). When you are fined, you might find yourself thinking “Iowa fortune so you can  Iowa”. Far better avoid that!

Iowa”. Far better avoid that!

sixteen. KANSAS: No permit needs having commercial loan providers. A permit is only you’ll need for lenders and you can “administered funds”, defined inside Ohio once the financing where in fact the Annual percentage rate is higher than 12%, as to that the debtor is one except that an enthusiastic business, the debt are priily otherwise domestic objectives, plus the amount borrowed doesn’t surpass $twenty five,100000. Kansas S.A good. 16a-1-301(17) (2019). Banks or other controlled depository establishments try excused from this certification needs. Ohio S.Good. 16a-1-301(44).

until brand new broker’s fee is totally contingent on the effective procurement from a loan regarding an authorized and who no percentage, other than a bona fide third-cluster percentage, is actually paid off through to the procurement.Kansas S.A. 50-1016(a) (5) (2019).

- Credit file, appraisals and research; and you can

- In case the mortgage is going to be covered by real estate, term inspections, a conceptual regarding name, term insurance, property survey and equivalent intentions.

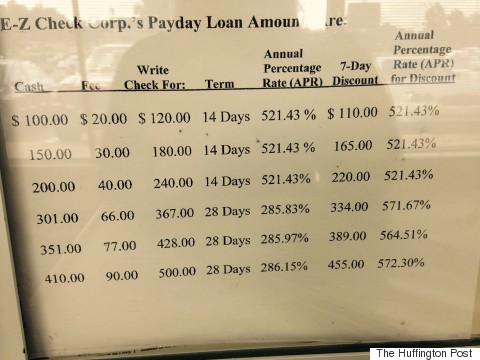

KENTUCKY: A personal bank loan company and make funds away from $fifteen,100000 otherwise quicker, for personal, family unit members, otherwise household have fun with, at the an interest rate higher than the usury rate (8%) ought a license

Remarkably, Kentucky is just one of the pair claims which obviously delineates one you don’t need to for a foreign financial institution to join up regarding the state to make finance out of out of county, or perhaps to care for an activity during the Kentucky to prosecute otherwise protect a lawsuit. KRS 286.2-670 (2009). Here is the statute:

Maine Consumer credit Code, Name nine, Blog post dos, Area 3

It’s mostly of the states you to demonstrably and indisputably offers lenders and you will agents the ability to conduct business off aside-of-state. A number of other states provides “similar” rules, but so it, centered on my search, try unequivocal. Bluish lawn bourbon, ponies and no licenses expected. Just what a lot more do you ask for?

18. LOUISIANA: Some other believe that doesn’t need a permit to make industrial loans. Mortgage agents, similarly, do not need a permit unless of course he’s and also make consumer funds. Los angeles. Changed Statute §§3572.dos and you may 3572.step three (2019). Overall you’ll predict regarding a new, local condition for example Louisiana, he or she is really protective of its people.

19. MAINE: Maine try rigorous within the certification standards, however,, gladly, it will not want permits to have commercial lenders. A number of other economic businesses, including personal bank loan servicers, pay check loan providers, and supervised loan providers (once again, people who provide so you’re able to consumers), do actually need permits.

20. MARYLAND: Nor does Maryland wanted a license to possess commercial loan providers. Although not, user loan providers do you desire permits. Md. Password Ann., Fin. Inst. §11-301(b)(5) (2018). The usury rates are 6% or 8% if there’s a written arrangement. Md. Code. Annm. Legislation §12-103(a)(1), but this is exactly inapplicable, and you may a loan provider can charge interest anyway if the mortgage are:

(i) A loan designed to a business; (ii) A commercial mortgage in excess of $fifteen,100 perhaps not covered because of the residential houses; otherwise (iii) A professional mortgage over $75,100000 covered by the domestic property.